Divine Insights Mar 2026

Dear Divine Clients & Friends

Before we begin, a brief note on current affairs. This month’s Divine Insights will be in two parts due to events unfolding concurrently that deserve more of our attention.

Today, we cover what’s playing out in the global energy markets as the price of oil reacts to the expanding conflict between the United States and Israel against Iran. It's messy and it affects us all.

Next week in part two, we turn to a developing financial hairball in private credit that is now in the early stages of being coughed up into the broader markets.

Different arenas. Same consequence; both affect how capital is moving through the global economy.

And don't worry, there's always some Good SH*T at the end!!

So, grab a coffee and let’s get into it.

Welcome to Divine Insights.

Each month we bring you a compendium of market news and data to assess the forces shaping markets and the economy.

At Divine, we focus on resilient strategy: values-aligned portfolios, global perspective, and clear thinking about wealth, business, and legacy.

This newsletter is for information purposes only & does not contain recommendations to buy or sell any securities.

Want to talk through your own financial picture?

I’m here.

POWER🔋🛢️

Oil: The Shock Transmission Mechanism

Fear moves through oil markets like a viral meme.

Political and military decisions are reflected almost immediately into commodity markets, where traders price the risk of supply disruption. Geopolitical instability, supply issues, or a stray comment from an energy minister can send crude prices moving within minutes.

The past two weeks illuminate how quickly that chain reaction unfolds.

Following U.S. and Israeli strikes inside Iran, and Iran’s response, traders immediately began pricing the risk to oil supply moving through the Persian Gulf. The focus was not simply on the conflict itself but on the energy infrastructure around it — tankers, pipelines, export terminals, and most importantly, open access to the Strait of Hormuz, as roughly twenty percent of the world’s oil supply moves through that narrow shipping corridor.

Oil is the primary fuel input of a long chain of economic activity, and higher oil prices affect:

gasoline and diesel

airline fuel

shipping and trucking costs

petrochemicals used in plastics and manufacturing

fertilizer and agricultural production

Credit: Divine Asset Mgt

The impact to energy costs cascades like dominos as airlines hedge fuel, freight rates adjust, and manufacturers face higher input costs. Agricultural production becomes more expensive because fertilizer and transportation costs rise. Consumers are impacted with all of it- the gas pump, heating and electric bills, and eventually in the price of goods moving through the economy.

Central banks are impacted immediately as energy spikes have a way of complicating the inflation outlook. "The net effect of an oil shock will still be some downward pressure on spending and employment, and some upward pressure on inflation." Fed Chair Powell said yesterday, “The thing I really want to emphasize is that nobody knows."

Clearly, none of this is new; energy shocks have shaped economic cycles for decades.

Oil Spikes in Recent History

Oil markets trade continuously through global futures exchanges, and prices adjust the moment traders believe supply could be threatened. Because the system runs with very little spare capacity, even small perceived disruptions can move prices quickly.

It may not feel like it right now, but historically, there have been larger and faster spikes.

1990 – Iraq Invades Kuwait

When Iraq invaded Kuwait in August 1990, oil prices doubled in roughly four months, jumping from about $17 to $36 per barrel.

Markets were suddenly pricing the loss of both Kuwaiti production and potential disruption to Saudi supply.

2008 – Commodity Supercycle Spike

During the global commodity boom, from approximately January to July 2008, oil climbed from about $90 to $147 per barrel in six months.

That move wasn’t war-driven but demand-driven as global growth and speculation pushed prices sharply higher.

The elevator down was even swifter; in September 2008, the Great Recession hit full force, and by December of that year oil was $30-35 a barrel.

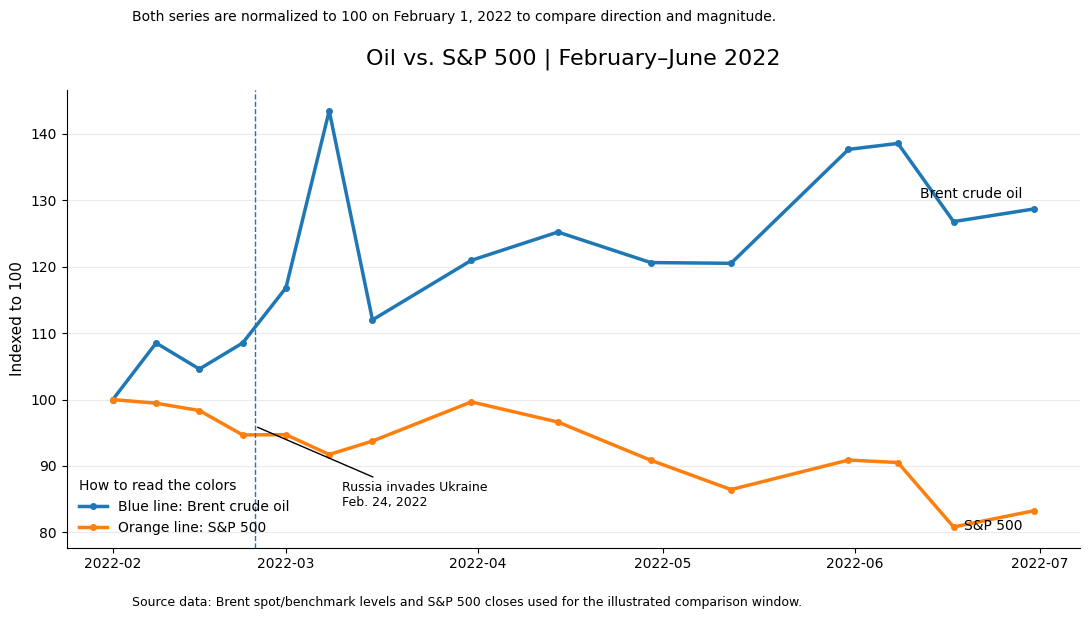

2022 – Russia Invades Ukraine*

When Russia invaded Ukraine, oil jumped from roughly $90 to $130 within two weeks — one of the fastest geopolitical repricings in recent decades.

Markets were reacting to potential sanctions on Russian energy exports.

*Russia/Crimea/the Soviet Union has invaded Ukraine many many times in history.

Why Oil Moves Faster Than Most Markets

The system runs with almost no slackGlobal demand sits around ~100 million barrels per day—and most of it has to show up every single day. Spare capacity exists, but it’s thin, concentrated, and not instantly deployable. Saudi Arabia and a handful of OPEC producers carry most of it.

Supply routes are concentratedIt moves through very specific arteries:

Strait of Hormuz

Suez Canal / SUMED pipeline

Turkish straits

Key pipelines into Europe and Asia

A disruption doesn’t need to happen—it just needs to be possible.

Futures markets price expectations. Traders don’t wait for the disruption — they price the possibility.

What Happens if Hormuz is blocked?

In the days surrounding the strikes this month, Brent crude moved from roughly $72 per barrel to above $100 - a 38% repricing of global energy risk in less than two weeks.

What happens if the flow of oil through that corridor slows or stops?

That corridor has gone from artery to capillary. Iran is moving just 1 to 1.7 million barrels a day into Pakistan, Turkey, India, and China, while roughly 95% of broader traffic has stopped. If this persists, we’re staring at inflation, contraction, and real strain on global food supply as fertilizer chains begin to crack.

In 2022 when Russian exports were at risk of sanctions, the impact was to just ~7–8% of globally traded oil supply; we are facing a 20% halt in flows. (see chart below)

Oil remains the fastest transmission channel from disruption to inflation, and from inflation to slower growth.

Why Do Oil Prices Still Matter? I thought the US was a net exporter…

The United States produces more oil than any country in the world.

According to the U.S. Energy Information Administration (EIA) and updated analyses using 2025 data:

Exports: ~10.7 million barrels per day

Imports: ~7.9–8.4 million barrels per day

So, we’re good, right?

Nope.

Oil (and other commodities) are priced in the global market, not a domestic one.

Barrels produced in Texas price in line with barrels produced in Saudi Arabia, Brazil, Norway, or Iraq. Traders price oil based on global supply and global demand, and those prices move instantly through futures markets in New York, London, and Singapore.

Even if the United States could supply every barrel it consumes, the price Americans pay would still be tied to the global market.

Energy independence does not mean price independence.

When markets believe even one or two million barrels per day could be disrupted — through sanctions, conflict, or shipping restrictions — prices adjust quickly and before the supply actually disappears.

Image Credit: Divine Asset Mgt

The Irony

Higher oil prices can actually benefit parts of the U.S. economy because the country is now a major energy producer and exporter.

Energy companies earn more revenue. They are not waiting on a tanker stuck in the strait of Harmuz- but because global prices jumped, they get to sell their oil at higher prices instantly.

Domestic drilling becomes more profitable. Drilling costs are the same, but they can sell the oil at much higher prices.

Export flows increase.

But for households and energy-intensive businesses, it increases our expenses and we feel the price increase immediately.

What is different today is the broader energy backdrop. At the same moment that geopolitical tension is tightening oil markets, electricity demand is rising rapidly across the global economy. Data centers, electrification, and industrial expansion are increasing the importance of reliable power systems in ways we have not seen before.

We’re entering a period of rising power demand, yet the very sources best positioned to meet it—solar, wind, storage—are being tangled in policy and regulatory drag.

While oil freaks out on the global stage, private credit is freaking out in the cushy back offices of private equity firms.

Next week, we move from in your face to behind the scenes. Oil shouts. Private credit whispers…until it doesn’t.

For years, capital has flowed into private markets with the promise of stability, yield, and insulation from volatility. But insulation has a cost: slower pricing, less transparency, and a tendency for problems to sit… and compound.

What’s starting to emerge is less a headline and more a hairball—a buildup of mismatched expectations, stale marks, and structures that haven’t been tested in a while. Plus some cat hair.

If oil is where risk is priced instantly, private credit is where risk lingers… and then surfaces all at once.

Now for the

Good Sh*t 📚

A shot of good news

🪻Its lighter outside at 6pm. The snow’s melting.

💲My friend Lizzette Muniz, Esq., an estate attorney and I are hosting a Spring Reset tonight at Gigi's in Rhinebeck, an intimate chat about investing and legacy. We are definitely going to do more of these around the Hudson Valley and the city--stay tuned!

🎧I highly recommend the podcast This Kaleidoscope Career hosted by my good friend Helen Jonsen, a story junkie, media expert and woman on a mission to showcase other women's career trajectories. Helen is so great at pulling our the fabulous tales of career growth, bumps and all. We never end up where we started out! Divine Asset Management is also a proud supporter of the show.

🌚Mercury turns direct (ends its retrograde phase) on March 20, 2026, bringing a conclusion to the period of communication, tech, and travel disruptions that began on February 26, 2026. As Mercury moves out of its Pisces retrograde, clarity returns, allowing for smoother decision-making and the resolution of lingering misunderstandings.

Yes, that's why your computer isn't working and you never received that email.

xo

Dani